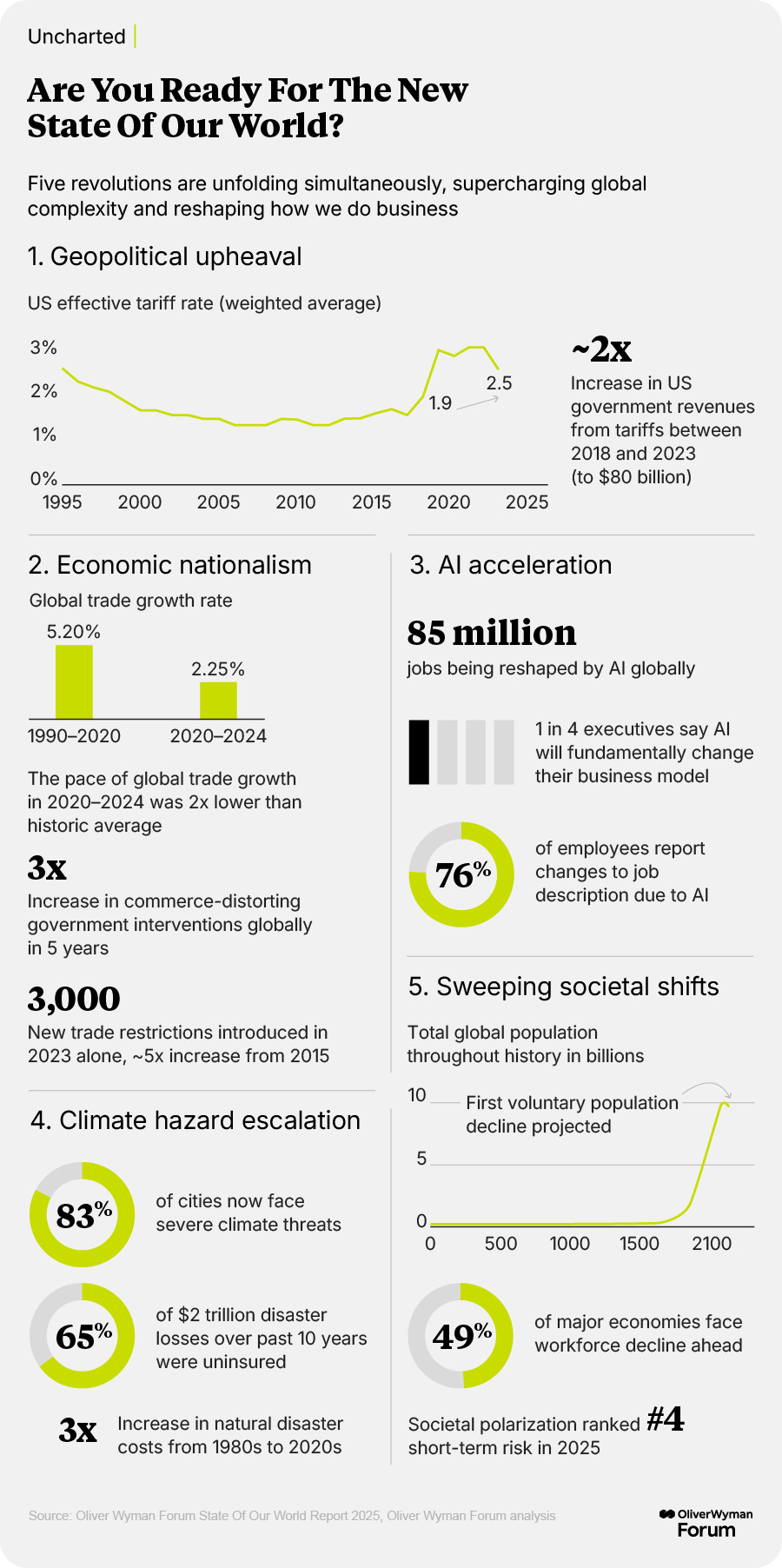

The norms governing global markets are changing rapidly and profoundly. Economic tools are being weaponized to an extent unparalleled in recent times, between both friendly and competitor nations alike and affecting a broad range of consumer goods as well as strategic sectors like aluminum and steel. CEOs need to adopt a geopolitics-first mindset to navigate the growing risks and make their supply chains more resilient.

Globalization isn’t dead. Trade in goods is projected to grow by 3% this year, slightly faster than in 2024, according to the World Trade Organization, while US imports and exports rose to record highs in 2024, according to the latest government figures. But the post-World War II consensus about the benefits of open trade and the framework of multilateral agreements that promoted it is on life support as a public backlash against globalization and increasing economic nationalism are driving the greatest government interference in markets in half a century, according to State Of Our World 2025, a new report from the Oliver Wyman Forum.

The new multipolar order

Further complicating the picture for policymakers and business leaders is the more-dispersed nature of economic power. It’s not just that the US-China economic rivalry has replaced the Cold War competition between the West and the former Soviet bloc. We have seen three distinct groups emerge during the past three years: a US-led coalition enforcing anti-Russia sanctions, a set of challengers opposing them (including Russia and China), and a powerful group of nations maintaining strategic neutrality. And these groups have their own internal tensions, with tariffs being threatened between ostensible allies and the Trump administration looking to negotiate with Moscow on an end to the war in Ukraine.

Today’s blocs interact with one another and are more evenly matched in economic power than in the past. Two-thirds of all nations now have larger trade volumes with China than with the United States, based on UN Comtrade data. And while the US remains the largest source of foreign direct investment globally, according to FDI Intelligence, China is the largest lender, according to Stanford’s Center on China’s Economy and Institutions.

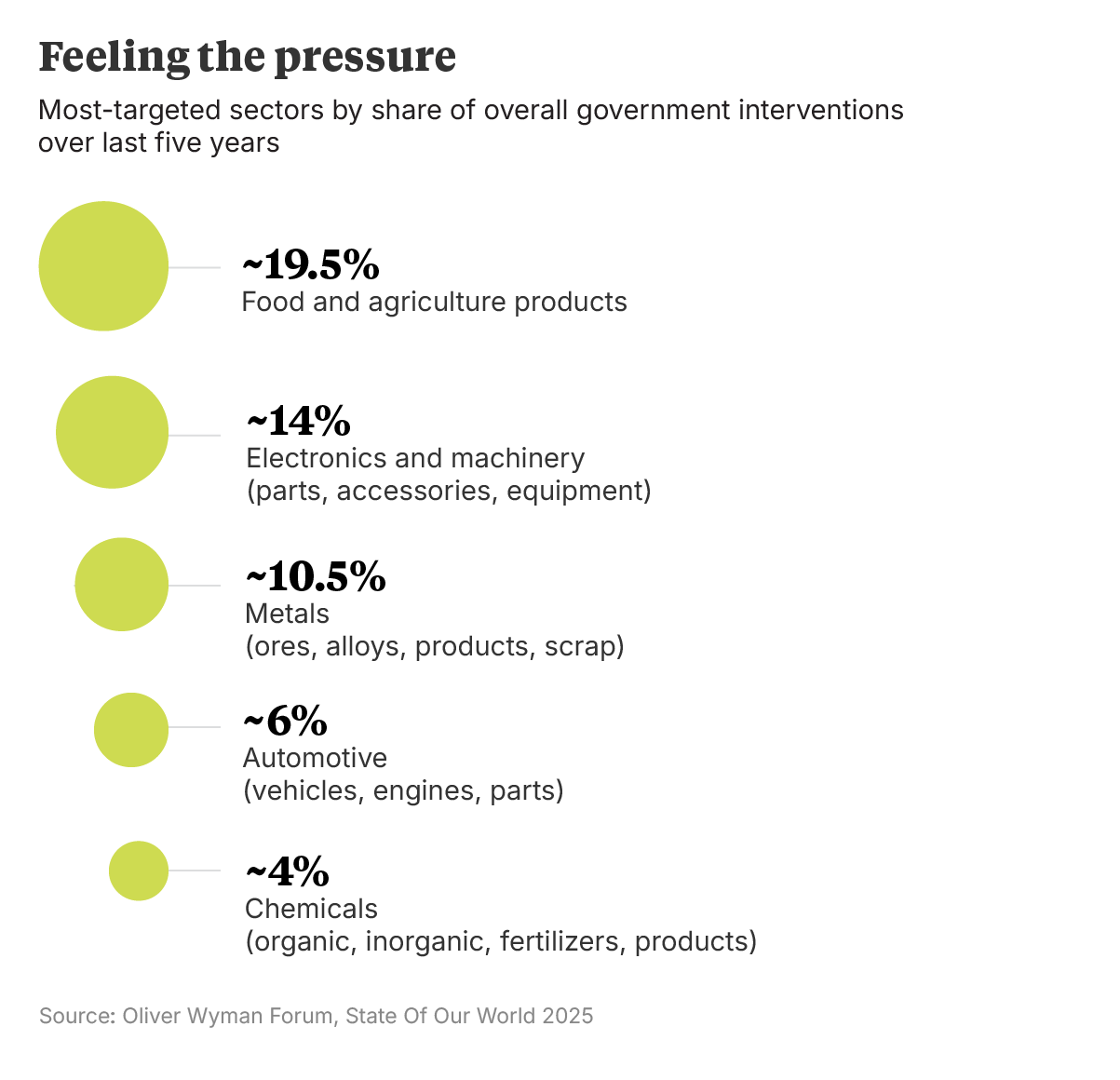

The heightened competition between countries and blocs has driven a three-fold increase in commerce-distorting interventions like tariffs, subsidies, and export controls in the past five years, driven primarily by the United States, China, and the European Union. These measures affect some of the most strategic sectors of the global economy.

Take a geopolitics-first approach

In this environment, CEOs have to make geopolitics a first consideration in their strategic planning rather than an afterthought.

Many get this. Eighty-six percent of leaders of large and midsized companies are already planning short-term actions to address geopolitics and protectionism, according to a recent survey of CEOs of New York Stock Exchange-listed companies by the Oliver Wyman Forum and NYSE. In addition, 43% of CEOs of large companies are running scenario-planning, war-gaming, or tabletop exercises around geopolitical events.

Yet most companies still aren’t bringing nuanced analysis of geopolitical drivers into long-term planning or using it early in the decision-making process on things like growth strategy, investment portfolios, supply-chain footprint, talent sourcing, and technology stacks. Only 24% of large companies are hiring talent with geopolitical expertise, according to the CEO survey.

Such capabilities might have seemed an extravagance a decade ago. Today, they’re a prerequisite for business outperformance in a world where politics drives markets.

Finding positive news on climate change can feel like searching for a needle in a haystack, what with temperatures and natural disasters rising and many countries and companies walking back on emissions reduction promises. Yet a new report finds that transparency around carbon emissions is helping to drive actual reductions at a significant number of large companies.

An evaluation of 6,800 companies representing 67% of global stock market capitalization finds that most still lack sufficient ambition to address climate change and nature loss, and only a third are on track to meet their emissions reduction targets, according to the CDP Corporate Health Check, a new report by the Carbon Disclosure Project (CDP), the World Economic Forum, and Oliver Wyman.

Yet 10% of the companies accounting for nearly 20% of global market cap are embedding Earth-positive decision-making across their businesses and taking tangible action to report full emissions and nature impacts across their value chains, the report finds. This enables them to establish effective climate and nature strategies with relevant targets and robust governance.

The companies evaluated in the CDP Corporate Health Check have cut greenhouse gas emissions from their own operations by 2% per year since 2022, while overall global emissions rose 1% annually.

The report identifies four key levers that the leading 10% of companies are pulling to drive Earth-positive decisions: creating climate transition plans aligned with the goal of limiting global warming to 1.5 degrees Celsius, putting an internal price on carbon, tying executive compensation to sustainability, and engaging with suppliers and customers on emissions reduction.

Executive pay is one of the most popular levers among the leaders on climate action. Eight in 10 use bonuses and other incentives for executives who help ensure companies meet their sustainability goals, and 87% actively engage with their value chains to reduce their carbon footprint.

Former Singaporean diplomat

“The most important statistic everyone should know is that in the CIA countries (China, India, and ASEAN), there were only 150 million people enjoying middle-class living standards in the year 2000. By 2020 that number had exploded 10 times, to 1.5 billion. And by 2030, it'll be 2.5 to 3 billion.”

Every month, we highlight a key piece of data drawn from three years’ worth of consumer research.