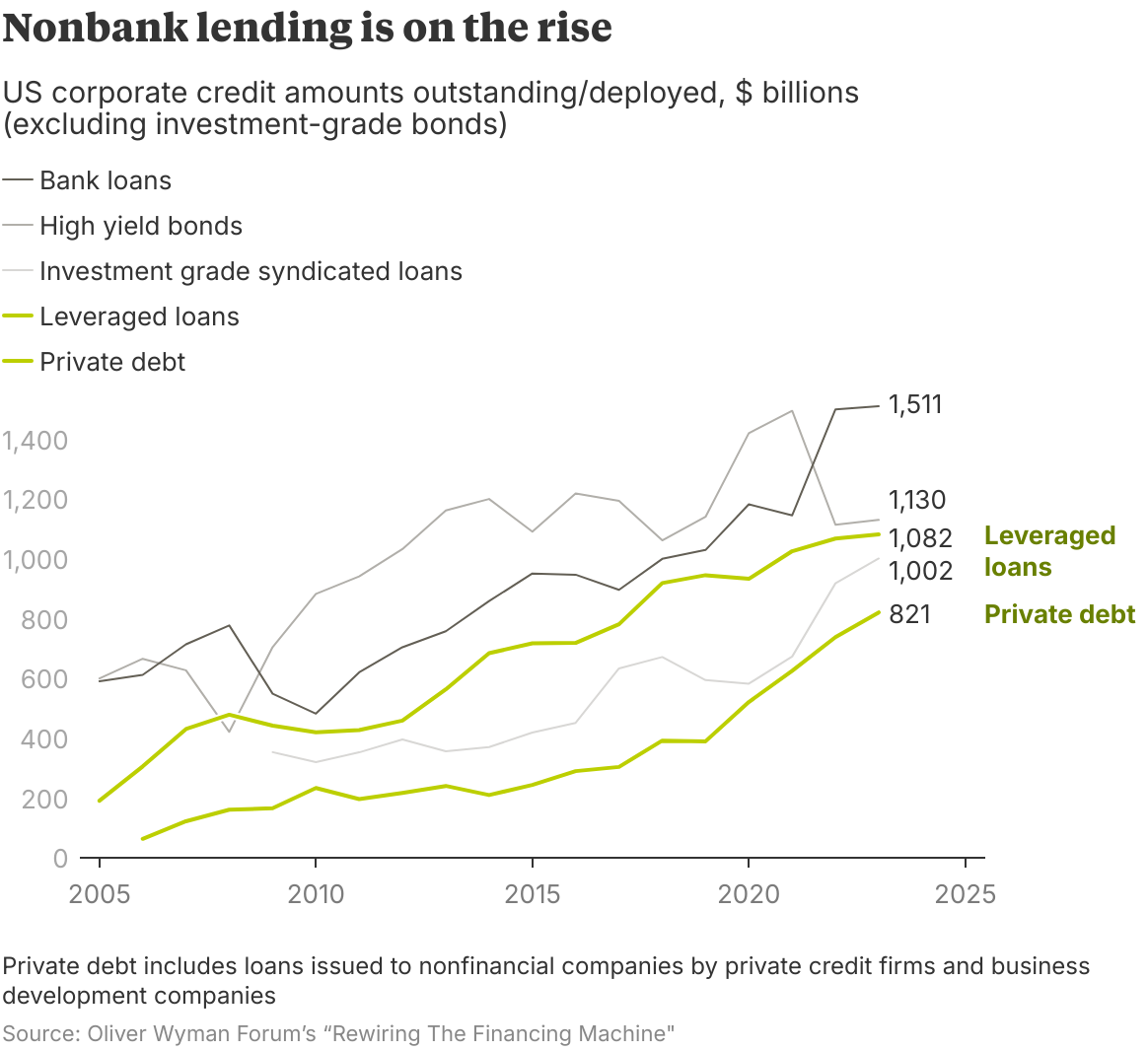

The corporate credit market is undergoing its biggest transformation since large companies started turning to the bond market instead of banks for financing in the 1980s. Private capital firms are gaining market share from banks through direct lending and products like collateralized loan obligations (CLOs), while hedge funds are making a splash in leveraged loans and corporate bonds. An explosion of fixed-income exchange-traded funds (ETFs) is helping retail investors get exposure to the bond market and enhancing liquidity.

These and related innovations are improving credit availability by expanding the options for borrowers and investors, which can foster more business investment, hiring, and economic growth, according to Rewiring The Financing Machine, a new report from the Oliver Wyman Forum. The innovations, which are most advanced in the United States but spreading to Europe and Asia, also reduce some risks by relying on long-term capital from insurers, pension funds, and other investors rather than banks, which tend to rely on deposits that can be withdrawn quickly in a crisis.

Yet the new corporate credit model carries hazards as well as benefits. Alternative credit providers are less regulated than banks and sometimes employ opaque structures, which can obscure risk. They also are increasing competition between credit providers, potentially leading to a lowering of standards, which can cause problems. And while new credit providers can add diversity and resiliency to the corporate credit market, the fact that banks are the biggest funders of these providers could undermine those benefits and leave the market vulnerable to a shock like the 2008-2009 global financial crisis.

Policymakers and industry executives need to better understand and monitor the risks and interconnections of the new corporate credit model to reduce the chance of a future crisis.

Measuring the credit transformation

Alternative credit providers and products have been around for decades but flourished in the wake of the global financial crisis. They typically offer higher yields than investment-grade debt securities, making them especially attractive to investors in the low-rate environment of the post-crisis years. Banks, meanwhile, had their risk appetite reduced by higher capital and liquidity requirements and other restrictions imposed after 2008.

As a result, once-niche areas of the credit markets have boomed. Private credit, which is financing provided by private capital firms and business development companies, has expanded by a factor of four globally since 2013, while leveraged loans, which are extended to borrowers with large debts or poor credit histories, have nearly doubled. The two segments now provide nearly 20% of US corporate credit.

This trend is spreading to other parts of the world. Private credit has grown by 17% a year since 2018 in Europe, where it now represents 2% of corporate credit, and by 20% a year in Asia.

Monitoring the risks

There are five key questions to consider in assessing the stability of today’s transformed corporate credit markets. Given that bank runs and margin calls can incite or exacerbate a financial crisis, policymakers and financial executives must ask themselves: What short-term liquidity promises are being made? It’s notable that US banks have extended $2 trillion in committed credit lines to nonbanks, with average utilization rates at about 50%.

Next, how are financial chains evolving and are they becoming more leveraged? Large US hedge funds hold more than $800 billion in credit derivatives, for example, while private equity firms put nearly $70 billion of debt on their portfolio companies in the first three quarters of this year. Such layers of exposure and leverage, along with a lack of transparency, make it difficult to accurately assess the associated risks.

How large are traditional institutions’ exposures to corporate credit and nonbanks? Banks have lost market share in corporate credit, but they are major lenders to nonbanks. US life insurers owned fully or partly by private capital firms have $600 billion in assets under management, representing 11% of the US life insurance industry. Policymakers and executives need to take a comprehensive view of all these avenues of exposure.

How will novel high-quality assets perform in a crisis? Regulated financial entities have a need for such assets, which are often created through securitization, but the process can generate products with different claims on corporate assets and pit the interests of senior debt holders against junior debt holders. Some of these structures are untested. For instance, one of the fastest-growing areas of the CLO market, reaching more than $115 billion in late 2023, invests in unrated private credit loans rather than leveraged loans.

Finally, how might a crisis play out, and what entities will have the capacity and risk appetite to become buyers in a crisis? Nonbanks have become more critical for market liquidity, but they lack the support channels from central banks that banks enjoy. There are also questions about whether banks or nonbanks have greater incentives and means to provide credit support to firms in a prolonged crisis.

Adapting regulation and supervision will take time, but policymakers should be vigilant for any signs of excessive buildup of risk. It is also critical that executives and investors proactively enforce market discipline by demanding transparency into fund holdings and leverage and conducting stress tests.

Closer scrutiny now can preserve the benefits of the market’s transformation and reduce the odds that today’s corporate credit boom lays the seeds for the next financial crisis.

The promise and the challenge of artificial intelligence (AI) — how to unleash it and where to deploy it — is arguably the biggest issue facing business executives today. They would do well to look at the healthcare industry, which is accelerating the adoption of AI.

Drug development is a prime example. Pfizer used AI with great success to develop a treatment for ALK-positive lung cancer, which accounts for about 5% of cases of the disease and strikes as many people under age 50 as over. The technology helped take the drug from clinical trial to regulatory approval in just four years instead of the usual decade, Lidia Fonseca, the company’s chief digital and technology officer, told executives attending the recent 2024 Oliver Wyman Health Innovation Summit. Pfizer expects generative AI to deliver nearly $1 billion in value across its operations in the near term, she added.

Attendees could walk through an immersive exhibit that included a simulation of how healthcare providers are using digital twins to advance precision medicine. Drawing on data from electronic health records, evidence-based studies, and patients themselves, the digital twin uses machine learning algorithms to enable patients and their doctors to see how various treatments are likely to work — before a drug is ever administered. The nascent technology shows promising results in oncology, cardiology, and other areas, and some projections suggest the healthcare market for digital twins will grow by a factor of 13, to $21 billion, by 2028.

Applications are improving care at the bedside, too. UC Davis Health, an academic health system in Northern California, has deployed an AI-based system that reads CT scans of suspected stroke patients from outlying hospitals to determine if they would benefit from immediate surgery. For those that would, UC Davis can helicopter patients from as far as 70 miles away and have them in an operating room within 40 minutes, said CEO David Lurbarsky, MD.

More broadly, Lurbarsky said AI has driven a 12% increase in clinician productivity and reduced some workloads by up to 30% through automation. As a result, doctors are getting to do more of what they love — direct patient care. But organizations need to redesign workflows to get the greatest benefits out of the technology, he cautioned. “If you layer AI on rotten processes, you end up with rotten results,” Lurbarsky said.

Organizations aiming to realize gains from AI and score early wins should engage a diverse set of leaders and articulate how AI fits into the organization’s overall strategy, according to Amy Waldron, Global Director, Healthcare and Life Sciences Solutions, Google Cloud. Demonstrating value from AI deployment is essential to maintaining momentum. And while there’s no perfect plan for deploying AI, the biggest risk leaders face is doing nothing.

Two actors simulate how a doctor can use a digital twin to project likely treatment outcomes for a cancer patient.

Every month, we highlight a key piece of data drawn from three years’ worth of consumer research.